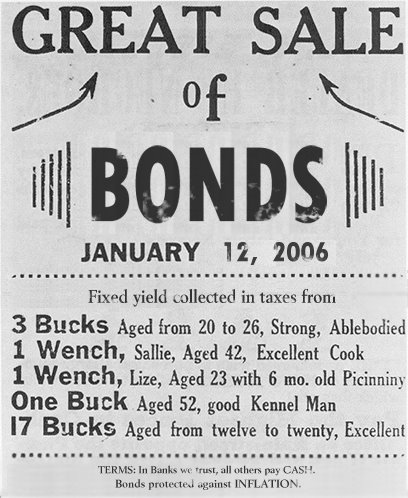

The US Slave Trade

Debt slaves, that is.

U.S. Treasury bond prices climbed after a successful auction of inflation-indexed debt.

"The TIPS auction was better than anticipated, especially the indirect bid."How is this auction any different from the slave auctions in days of old?

[T]he primary catalyst for the market's upward thrust was the auction of $9 billion in 10-year inflation-protected securities.

The sale garnered a high yield of 2.025 percent and drew 1.85 bids per dollar of debt on offer, up from the 1.78 average of the two 10-year TIPS auctions in 2005.

It isn't.

Not only is the bond an obligation, on the tax payer, to pay the value of the bond plus interest over the life of the bond, but this particular bond is inflation-indexed, which means that while our dollars are decreasing in value, theirs are increasing in value.

Coincidence? No. Try causal relationship.

[image edited by vper1]

posted by qrswave @ Thursday, January 19, 2006

![]()

3 Comments:

Yes Morpheus I think it does make them feel better. Another screw job on us the tax payers. And who okayed this piece of work thats what I would like to know.

Sean

Is a TIB callable? If not - then it is one of the greatest scams our Treasury has ran for a long time. I wonder how CMO IOETTES will be doing near term. This calls for another new financial product - the inversely floating inverse floater. It's a hedge against itself - no revenue - but the curves are cool to watch!

The Inflation Indexed Treasury has been around for a while. I first heard of it when 30 year treauries paid coupons in the teens - and people were still reluctant to buy them. The reason it was invented was simple. When Tresuries are bought and sold, the coupon rate remains the same. If someone really wanted to buy a good rate, he would pay a premium, say a 1.20$ for every 1.00$ (Principal + 20%). If a guy really needed to sell his, he might sell it at 0.80$ on the dollar. A loss of of 20 cents on par (par=1.00$). The price / rate volatility of the mid nineties weakened demand for US notes. So someone came up with the TIB (Tiered Index Bond). It can be a hedge. If your business has inflation risks, the additional return from the TIB would help recover the losses.

But the problem is - speculators will not buy it as a cost recovery hedge, they will, instead, buy (and then sell) because they are betting that inflation will go up. At some point the music stops and somebody is stuck with a bond they will have to wait till it matures to get the par prinicpal back. They may have taken a loss on the purchase price and paid par plus a premium, and would also risk a "cash" loss. They will be stuck with a bond in a low inflation market that is not paying interest or they will have to sell it at pennies on the dollar.

The big problem is the return is paid in the same worthless dollars the investor is betting against.

And if inflation goes crazy - mortgages will default. BTW: Mortgage Principal is insured by the full faith and credit of the US Government. When a loan defaults, the US treasurey (that be you and me) pays the lender the principal balance on the note. In a high default environment them TIBs could look good - but you'd be getting back dollars.

It's good to be a lender - and this stuff goes back to Balfour, Brandies, Wilson through the Federal Reserve and finally the magnificent fraud of synergist banking.

Post a Comment

<< Home